Recap: Widespread labor shortages, overwhelmed supply chains, and mounting inflation pressures have come to be unfortunate hallmarks of the economic recovery from the pandemic-induced recession. Many of these headwinds, however, have been side effects from the unexpectedly strong bounce back in overall economic growth experienced over the past 18 months.

In terms of the current public health situation, COVID case counts have come down considerably from the summer surge brought on by the Delta variant. Rising vaccination rates and an expanding toolbox of therapeutics are reasons to be optimistic that future iterations of the virus will be less impactful from an economic perspective.

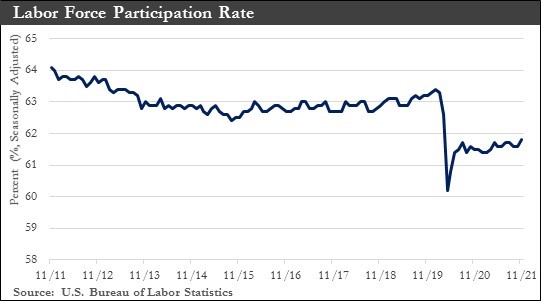

Labor shortages have weighed on businesses, but October’s strong employment report has indicated that the loss of momentum during the Delta wave was not as substantial as initially thought. Labor force participation, on the other hand, has been sluggish to return to pre-pandemic form, but improvement is forecast on this front in the year ahead.

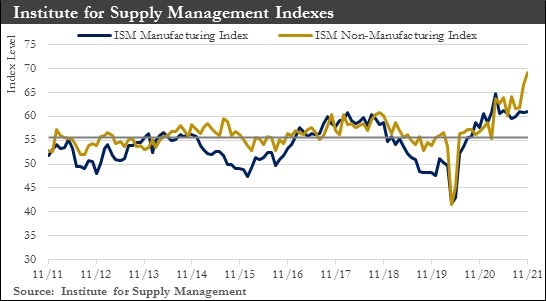

Some good news for the U.S. economy – the ISM services index suggests that the service sector is running on all cylinders. The index rose to 66.7 in October (from 61.9 in September) – the highest level on record.

While services were driving ahead, expansion in the manufacturing sector cooled in October. The ISM manufacturing index declined marginally to 60.8 from 61.1 in September. Supply-chain bottlenecks and labor shortages have hampered manufacturing output.

U.S. retail sales rose by 1.7% in October, a sign that consumers are willing to spend more headed into the holidays despite rising inflation. The combination of strong demand snarled supply chains, higher prices, and an unbalanced labor market has made for an unusual holiday season where record sales may be accompanied by shortages and long waits for goods.

Further evidence has shown that U.S. domestic demand is ahead of much of the rest of the world; the U.S. trade deficit widened again in September, reaching a record level for the third consecutive month. The widening deficit was driven by a 3% decrease in exports and a 0.6% increase in imports. With ongoing evidence of demand resiliency, the Fed is likely to continue to signal the gradual withdrawal of policy support. The first hike in the federal funds rate should follow shortly after the end of asset purchases, with at least one more to come before the end of 2022.

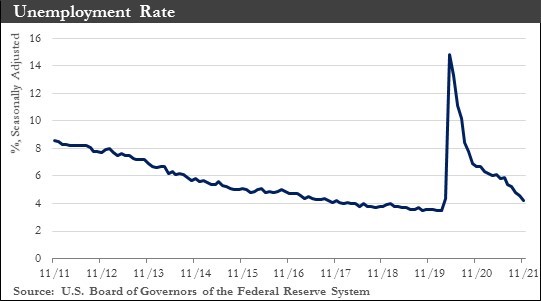

Labor Market: The U.S. job market shook off its malaise in October as hiring picked up, with payrolls gaining 531,000 jobs while employers further boosted wages, a sign the economy has been rebounding from the Delta variant wave but remaining restrained by a depleted labor force.

The unemployment rate fell to 4.6% in October from 4.8% a month earlier and is down by more than half a percentage point in just two months. The U.S. still has four million fewer jobs than in February 2020, the month before the pandemic shut down much of the economy, and the unemployment rate has remained higher than the pre-pandemic level of 3.5%.

One of the longer-lasting impacts of the pandemic shock has been a persistent decline in the number of people participating in the labor market. A steep drop in the labor force participation rate following the COVID-19 shock has left the U.S. labor force roughly three million people smaller. How quickly these people return has been a central economic question.

The scarcity of workers has been owed to a confluence of factors including expanded unemployment benefits, retirements, child-care issues, and health concerns. Aside from the pickup in retirements, which is unlikely to be reversed, most of these other factors will more than likely see improvement in the year ahead.

The exit of millions of older workers who have decided to retire early rather than try to get their jobs back has been a big factor behind the smaller labor force. About 40% of Americans missing from the labor force now are over the age of 55 and roughly one-third are older than 65. Before the recession, this group was a key source of labor force growth. People can and do return to the workforce from retirement, but the odds diminish with every passing year.

Among core working-age people (25 to 54), more women left the workforce than men. The difference in participation has been most notable among Americans in their late twenties. For young people below the age of 25, the biggest decline in participation has been among college-aged students. Changes to campus life brought on by the pandemic have likely contributed to this phenomenon.

While the labor force participation rate should rebound, it may take several years before key demographic groups return to their pre-recession levels. In the meantime, relatively little growth in the population under 65 years of age will mean labor force growth would remain below historical norms.

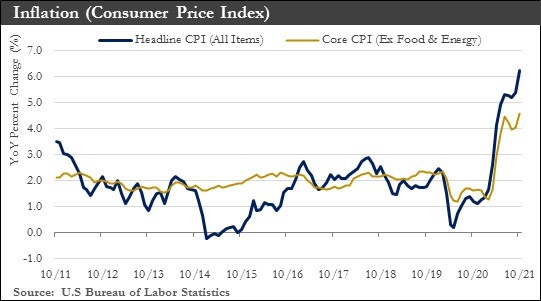

Inflation: The scorching pace of inflation continued in October, with the Consumer Price Index jumping another 0.9%. Prices over the past year were up 6.2%, the strongest one-year gain in more than 30 years. Core inflation also picked up to a 0.6% m/m increase, from 0.2% in September. That saw the year-on-year rate of core inflation pick up to 4.6%, also a 30-year high.

Unusually high demand—boosted by government stimulus and an improved job market has been a crucial factor driving higher inflation. Businesses have also passed on higher costs to consumers. Companies have struggled to get materials and are delaying orders, adding to demand pressures. The shortage of workers needed to meet consumer demand has also put upward pressure on wages, adding to companies’ motivations for raising prices to offset higher labor costs. Higher food and energy prices - driven up by pandemic-related production snags, weather, and geopolitical factors- have equally spurred inflation.

The inflation surge has complicated the Federal Reserve’s strategy for unwinding easy-money policies the central bank imposed early in the pandemic. It has also emerged as a political factor affecting the Biden administration’s economic agenda.

Fed officials have watched inflation measures closely to gauge whether the recent jump in prices will be temporary or longer-lasting. One such factor is consumer expectations of future inflation, which could prove self-fulfilling as households are more likely to demand higher wages and accept higher prices in anticipation of further price hikes.

Inflation should push even higher in the months ahead before starting to subside around the second quarter of next year. However, with supply chains likely to be affected well into next year and service-sector prices trending higher, inflation may well not resemble anything close to the Fed's goal until 2023.

Federal Reserve: The central bank approved plans to begin scaling back its bond-buying stimulus program in November and end it by June, a key step toward withdrawing pandemic-driven economic support amid a recent inflation surge.

As expected, the Federal Reserve Open Market Committee (FOMC) kept the federal funds rate in the 0% to 0.25% range. More importantly, it also announced a reduction in its Quantitative Easing (QE) asset purchase program from its current schedule of $80 billion per month in Treasuries and $40 billion per month in agency mortgage-back securities. The taper schedule will reduce "the monthly pace of its net asset purchases by $10 billion for Treasury securities and $5 billion for agency mortgage-backed securities" beginning late in November.

This is the first step in the removal of pandemic-induced monetary policy support. With the initiation of a taper in November, balance sheet expansion will likely end by June 2022. By that time, employment should be above pre-pandemic levels. With inflation set to remain above the 2% target through next year, the Fed should execute rate hikes in the second half of 2022.

And just before Thanksgiving, Jerome Powell was renominated by President Biden for a second term as Chairman of the Federal Reserve. Early reaction to this announcement indicates the market expects a second Powell term to be less accommodative as monetary stimulus is withdrawn from the economy and interest rates rise.

Global Economy: The global economy has faced several issues in recent months. The economic effects of the Delta variant as well as China's softening growth outlook have proven to be more severe than initially expected. COVID-related issues have continued to weigh on the outlook for the global economy, while virus restrictions, President Xi’s “common prosperity” plans, as well as a significant deceleration in the local real estate sector, have resulted in a sharp slowdown in China’s economy.

Global economic growth has remained on a downward trajectory. To that point, the global economy should grow 5.8% in 2021 and 4.2% in 2022.

China has been the largest contributor to the softer global growth outlook, as the country still operates under restrictions given persistent COVID outbreaks. In addition, Chinese authorities have been rationing energy, which has weighed on manufacturing production. COVID and energy rationing have contributed to slower Q3 growth and have also been a driving force of the manufacturing PMI falling into contraction territory in October.

Local financial markets have also remained volatile amid President Xi's common prosperity plans, and China's decelerating real estate sector has placed pressure on the economy. All of these challenges together have slowed the Chinese economy to 8% growth this year. Risks around this forecast have tilted towards even slower growth.

Despite an outlook for slower global growth, central banks around the developed world will continue to tighten monetary policy. Emerging market central banks could continue raising policy rates at a somewhat aggressive pace. Financial markets may be priced for too much tightening. Over time, markets will adjust to a slower pace of interest rate hikes from foreign central banks and for foreign currencies to weaken over the short term. This financial market adjustment has been a key factor for a stronger U.S. dollar through the end of Q1-2022. Over the longer term, the US dollar should gradually weaken.

Outlook: Strong, above trend, economic growth is expected over the next couple of years. The sources of growth have been shifting, however, away from consumption and more toward production, which has lagged since the onset of the pandemic.

Despite a marked slowdown in the third quarter, real GDP is on pace to expand 5.5% in 2021. Expansion is expected to moderate from there, but healthy household and corporate balance sheets should help drive an above-trend pace of growth. Real GDP is expected to rise at least 4.0% in 2022.

Supply chain blockages that have been hampering many parts of the economy are expected to begin to clear up over the course of next year and to be functioning more or less normally in 2023. While the holiday season will likely be a strain in the near term, logistics networks presumably will be under far less stress moving into 2022.

Even though supply chains are expected to run more smoothly in 2023, there is little evidence that inflationary pressures will ease in the foreseeable future. The Consumer Price Index (CPI) rose 6.2% year over year in October, and inflation appears set to push even higher over the next few months. CPI is expected to rise at least 5.0% during 2022.

With inflation likely to remain hot and the labor market firmly on the path toward recovery, an earlier lift-off for the federal funds rate is in the cards. The FOMC will likely raise the target range for the federal funds rate by 25 bps in Q3-2022 and another 25 bps in Q4-2022.

Job growth is expected to remain steady because of several factors. Delta cases have declined. Employers desperate to hire to meet strong demand from consumers are rapidly raising wages, dangling bonuses, and offering more flexible work hours. And households are spending down savings that had been boosted by federal stimulus money and extra unemployment benefits.

This Newsletter was produced for Atlantic Union Bank Wealth Management by Capital Market Consultants, Inc.

In terms of the current public health situation, COVID case counts have come down considerably from the summer surge brought on by the Delta variant. Rising vaccination rates and an expanding toolbox of therapeutics are reasons to be optimistic that future iterations of the virus will be less impactful from an economic perspective.

Labor shortages have weighed on businesses, but October’s strong employment report has indicated that the loss of momentum during the Delta wave was not as substantial as initially thought. Labor force participation, on the other hand, has been sluggish to return to pre-pandemic form, but improvement is forecast on this front in the year ahead.

Some good news for the U.S. economy – the ISM services index suggests that the service sector is running on all cylinders. The index rose to 66.7 in October (from 61.9 in September) – the highest level on record.

While services were driving ahead, expansion in the manufacturing sector cooled in October. The ISM manufacturing index declined marginally to 60.8 from 61.1 in September. Supply-chain bottlenecks and labor shortages have hampered manufacturing output.

U.S. retail sales rose by 1.7% in October, a sign that consumers are willing to spend more headed into the holidays despite rising inflation. The combination of strong demand snarled supply chains, higher prices, and an unbalanced labor market has made for an unusual holiday season where record sales may be accompanied by shortages and long waits for goods.

Further evidence has shown that U.S. domestic demand is ahead of much of the rest of the world; the U.S. trade deficit widened again in September, reaching a record level for the third consecutive month. The widening deficit was driven by a 3% decrease in exports and a 0.6% increase in imports. With ongoing evidence of demand resiliency, the Fed is likely to continue to signal the gradual withdrawal of policy support. The first hike in the federal funds rate should follow shortly after the end of asset purchases, with at least one more to come before the end of 2022.

Labor Market: The U.S. job market shook off its malaise in October as hiring picked up, with payrolls gaining 531,000 jobs while employers further boosted wages, a sign the economy has been rebounding from the Delta variant wave but remaining restrained by a depleted labor force.

The unemployment rate fell to 4.6% in October from 4.8% a month earlier and is down by more than half a percentage point in just two months. The U.S. still has four million fewer jobs than in February 2020, the month before the pandemic shut down much of the economy, and the unemployment rate has remained higher than the pre-pandemic level of 3.5%.

One of the longer-lasting impacts of the pandemic shock has been a persistent decline in the number of people participating in the labor market. A steep drop in the labor force participation rate following the COVID-19 shock has left the U.S. labor force roughly three million people smaller. How quickly these people return has been a central economic question.

The scarcity of workers has been owed to a confluence of factors including expanded unemployment benefits, retirements, child-care issues, and health concerns. Aside from the pickup in retirements, which is unlikely to be reversed, most of these other factors will more than likely see improvement in the year ahead.

The exit of millions of older workers who have decided to retire early rather than try to get their jobs back has been a big factor behind the smaller labor force. About 40% of Americans missing from the labor force now are over the age of 55 and roughly one-third are older than 65. Before the recession, this group was a key source of labor force growth. People can and do return to the workforce from retirement, but the odds diminish with every passing year.

Among core working-age people (25 to 54), more women left the workforce than men. The difference in participation has been most notable among Americans in their late twenties. For young people below the age of 25, the biggest decline in participation has been among college-aged students. Changes to campus life brought on by the pandemic have likely contributed to this phenomenon.

While the labor force participation rate should rebound, it may take several years before key demographic groups return to their pre-recession levels. In the meantime, relatively little growth in the population under 65 years of age will mean labor force growth would remain below historical norms.

Inflation: The scorching pace of inflation continued in October, with the Consumer Price Index jumping another 0.9%. Prices over the past year were up 6.2%, the strongest one-year gain in more than 30 years. Core inflation also picked up to a 0.6% m/m increase, from 0.2% in September. That saw the year-on-year rate of core inflation pick up to 4.6%, also a 30-year high.

Unusually high demand—boosted by government stimulus and an improved job market has been a crucial factor driving higher inflation. Businesses have also passed on higher costs to consumers. Companies have struggled to get materials and are delaying orders, adding to demand pressures. The shortage of workers needed to meet consumer demand has also put upward pressure on wages, adding to companies’ motivations for raising prices to offset higher labor costs. Higher food and energy prices - driven up by pandemic-related production snags, weather, and geopolitical factors- have equally spurred inflation.

The inflation surge has complicated the Federal Reserve’s strategy for unwinding easy-money policies the central bank imposed early in the pandemic. It has also emerged as a political factor affecting the Biden administration’s economic agenda.

Fed officials have watched inflation measures closely to gauge whether the recent jump in prices will be temporary or longer-lasting. One such factor is consumer expectations of future inflation, which could prove self-fulfilling as households are more likely to demand higher wages and accept higher prices in anticipation of further price hikes.

Inflation should push even higher in the months ahead before starting to subside around the second quarter of next year. However, with supply chains likely to be affected well into next year and service-sector prices trending higher, inflation may well not resemble anything close to the Fed's goal until 2023.

Federal Reserve: The central bank approved plans to begin scaling back its bond-buying stimulus program in November and end it by June, a key step toward withdrawing pandemic-driven economic support amid a recent inflation surge.

As expected, the Federal Reserve Open Market Committee (FOMC) kept the federal funds rate in the 0% to 0.25% range. More importantly, it also announced a reduction in its Quantitative Easing (QE) asset purchase program from its current schedule of $80 billion per month in Treasuries and $40 billion per month in agency mortgage-back securities. The taper schedule will reduce "the monthly pace of its net asset purchases by $10 billion for Treasury securities and $5 billion for agency mortgage-backed securities" beginning late in November.

This is the first step in the removal of pandemic-induced monetary policy support. With the initiation of a taper in November, balance sheet expansion will likely end by June 2022. By that time, employment should be above pre-pandemic levels. With inflation set to remain above the 2% target through next year, the Fed should execute rate hikes in the second half of 2022.

And just before Thanksgiving, Jerome Powell was renominated by President Biden for a second term as Chairman of the Federal Reserve. Early reaction to this announcement indicates the market expects a second Powell term to be less accommodative as monetary stimulus is withdrawn from the economy and interest rates rise.

Global Economy: The global economy has faced several issues in recent months. The economic effects of the Delta variant as well as China's softening growth outlook have proven to be more severe than initially expected. COVID-related issues have continued to weigh on the outlook for the global economy, while virus restrictions, President Xi’s “common prosperity” plans, as well as a significant deceleration in the local real estate sector, have resulted in a sharp slowdown in China’s economy.

Global economic growth has remained on a downward trajectory. To that point, the global economy should grow 5.8% in 2021 and 4.2% in 2022.

China has been the largest contributor to the softer global growth outlook, as the country still operates under restrictions given persistent COVID outbreaks. In addition, Chinese authorities have been rationing energy, which has weighed on manufacturing production. COVID and energy rationing have contributed to slower Q3 growth and have also been a driving force of the manufacturing PMI falling into contraction territory in October.

Local financial markets have also remained volatile amid President Xi's common prosperity plans, and China's decelerating real estate sector has placed pressure on the economy. All of these challenges together have slowed the Chinese economy to 8% growth this year. Risks around this forecast have tilted towards even slower growth.

Despite an outlook for slower global growth, central banks around the developed world will continue to tighten monetary policy. Emerging market central banks could continue raising policy rates at a somewhat aggressive pace. Financial markets may be priced for too much tightening. Over time, markets will adjust to a slower pace of interest rate hikes from foreign central banks and for foreign currencies to weaken over the short term. This financial market adjustment has been a key factor for a stronger U.S. dollar through the end of Q1-2022. Over the longer term, the US dollar should gradually weaken.

Outlook: Strong, above trend, economic growth is expected over the next couple of years. The sources of growth have been shifting, however, away from consumption and more toward production, which has lagged since the onset of the pandemic.

Despite a marked slowdown in the third quarter, real GDP is on pace to expand 5.5% in 2021. Expansion is expected to moderate from there, but healthy household and corporate balance sheets should help drive an above-trend pace of growth. Real GDP is expected to rise at least 4.0% in 2022.

Supply chain blockages that have been hampering many parts of the economy are expected to begin to clear up over the course of next year and to be functioning more or less normally in 2023. While the holiday season will likely be a strain in the near term, logistics networks presumably will be under far less stress moving into 2022.

Even though supply chains are expected to run more smoothly in 2023, there is little evidence that inflationary pressures will ease in the foreseeable future. The Consumer Price Index (CPI) rose 6.2% year over year in October, and inflation appears set to push even higher over the next few months. CPI is expected to rise at least 5.0% during 2022.

With inflation likely to remain hot and the labor market firmly on the path toward recovery, an earlier lift-off for the federal funds rate is in the cards. The FOMC will likely raise the target range for the federal funds rate by 25 bps in Q3-2022 and another 25 bps in Q4-2022.

Job growth is expected to remain steady because of several factors. Delta cases have declined. Employers desperate to hire to meet strong demand from consumers are rapidly raising wages, dangling bonuses, and offering more flexible work hours. And households are spending down savings that had been boosted by federal stimulus money and extra unemployment benefits.

This Newsletter was produced for Atlantic Union Bank Wealth Management by Capital Market Consultants, Inc.

Sources: Department of Labor, Department of Commerce, Institute for Supply Management, Morningstar, Bloomberg, Peoples Bank of China, Federal Reserve of Chicago, John Hopkins University

Disclosures:

Past performance quoted is past performance and is not a guarantee of future results. Portfolio diversification does not guarantee investment returns and does not eliminate the risk of loss. The opinions and estimates put forth constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Securities are not insured by FDIC or any other government agency, are not bank guaranteed, are not deposits or a condition to any banking service or activity, are subject to risk and may lose value, including the possible loss of principal.

Atlantic Union Bank Wealth Management is a division of Atlantic Union Bank that offers asset management, private banking, and trust and estate services. Securities are not insured by the FDIC or any other government agency, are not deposits or obligations of Atlantic Union Bank, are not guaranteed by Atlantic Union Bank or any of its affiliates, and are subject to risks, including the possible loss of principal. Deposit products are provided by Atlantic Union Bank, Member FDIC.