Recap: The U.S. economy grew at a solid 2.9% annual rate last quarter but entered this year with less momentum as rising interest rates and still-high inflation weighed on demand.

Ongoing strength in the labor market has helped corroborate the view that the economy is on a positive growth path at present. Nonfarm payrolls increased by 223,000 in December. Slower inflation over the past few months, led by falling energy prices and normalizing prices for pandemic-hit sectors such as autos and airfares, has likely played a role in sustaining the momentum of the economy.

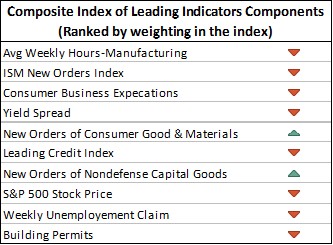

These recent developments have been encouraging signs that the U.S. economy could avoid a recession while getting inflation back to a more acceptable rate. However, the road ahead could still be challenging. The buoyancy of the labor market stands in contrast to the Institute for Supply Management’s (ISM) manufacturing and services indices, which have been pointing to a downswing in economic activity soon. The ISM indices have fallen into contractionary territory, the housing market has materially retrenched, households have taken on credit card debt and labor demand has shown signs of cooling.

U.S. consumers cut back on retail spending at the height of the holiday season spending less on vehicles, popular gifts, and furniture. Retail sales fell 1.1% in December which was the sharpest pace of 2022. This marked a dismal end to the holiday shopping season as concerns about a slowing economy pinched American consumers. Household balance sheets have not been as healthy as they were a year ago amid lower asset prices, dwindling "excess" savings, and rapidly rising credit card debt. Financial conditions have eased when viewed through the recent moves in stock prices and credit spreads, but they remained well off their all-time highs/tights, and the Treasury yield curve has still been deeply inverted across numerous maturity points.

Furthermore, core inflation has remained above the Federal Reserve's 2% inflation target, and policymakers at the Fed believe there is still work to be done on the inflation fight. As a result, monetary policy has appeared poised to become more restrictive in the months ahead, and a full pivot to rate cuts remains a long way off. The lagged effect of past policy tightening in combination with the rate hikes and balance sheet reductions still to come should impart a slowing effect on the U.S. economy as 2023 progresses.

The U.S. international trade deficit narrowed sharply to $61.5B in November, the narrowest in over two years. The narrowing was the result of a collapse in imports. While all major categories declined, the pullback in consumer goods led to the drop. While some volatile factors could explain the sharp decline, broad weakness would suggest the transition away from goods purchases by U.S. consumers may be starting to show up in import activity. While this could present some possible upside to Q4 U.S. GDP growth as the deficit falls, the details would suggest economic weakness has also started to show up in trade flows.

On balance, a recession should begin in the United States in the second half of this year, although a slightly milder one than previously expected.

On the political front, concerns about the government's ability to pay its debts resurfaced as the Treasury Department was forced to begin taking extraordinary measures to keep paying the government’s bills. By suspending certain additional investments, the Treasury would buy Congress more time – likely until June - to negotiate a resolution on how to increase the debt ceiling.

The global economy overall has shown signs of losing momentum as well. Global economic demand weakened toward the end of 2022 under the weight of high inflation and rising interest rates, combined with challenges caused by the war in Ukraine and Covid-19 lockdowns in China.

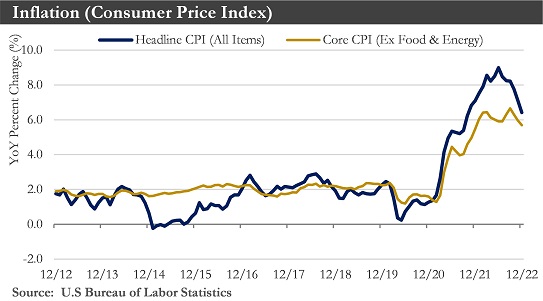

Inflation: U.S. inflation eased in December for the sixth straight month as the Federal Reserve aggressively raised interest rates and the economy showed signs of cooling. The consumer-price index rose 6.5% in December from a year earlier, down from 7.1% in November and well below a 9.1% peak in June.

Core CPI climbed 5.7% in December from a year earlier, easing from a 6% gain in November. Core prices increased at a 3.1% annualized rate in the three months that ended in December, the slowest pace in more than a year and down from 7.9% in June.

These figures added to signs that inflation has turned a corner following last year’s surge. Goods prices, a key driver of inflation over the past year and a half, fell for the third straight month in December. Improving supply chains and reduced demand have relieved price pressures on goods, but service prices continued to climb in part because of wage gains in a tight labor market. High wage growth could keep consumers flush with cash and companies eager to raise prices to compensate, holding inflation above the Fed’s 2% target. Taming services inflation will be the Fed’s biggest challenge this year.

Labor market: Employers added 4.5 million jobs in 2022 showing that the labor market remained a source of U.S. economic strength at a time of high inflation, climbing interest rates, and uneven growth. The U.S. economy added 223,000 jobs in December. The unemployment rate ticked lower to 3.5% – returning to its 50-year low. The participation rate edged higher rising to 62.3% and ending the year about where it started. Average hourly earnings rose 0.3% month-over-month (m/m) – a deceleration from the 0.4% m/m gain recorded in November. Compared to December 2021, wage growth was up 4.6%. The continuing effects of the economy’s bounce back following Covid-19 lockdowns, a wave of retirements early in the pandemic, and strong household spending have pushed up employer demand for workers—and paychecks—when those workers have been scarce. Wage growth has been identified by the Federal Reserve as the primary source fueling higher inflation across many of the labor-intensive service sectors.

Hiring had been resilient throughout 2022 despite an economy that has slowed alongside the Federal Reserve’s aggressive pace of interest rate increases aimed at bringing down inflation. However, some recent data and a wave of tech and finance industry layoffs have suggested the labor market, while still vibrant, may be starting to lose momentum and gains could reverse in the year ahead.

But there are still 1.7 job openings for every person actively looking for work. With labor force growth showing little improvement this past year, labor demand will need to slow considerably more to restore balance in the labor market and cool wage pressures.

This year could be more challenging for the labor market as the economy absorbs the impact of slowing global growth and the lagged effect of higher interest rates.

Housing: The clearest impact of Fed tightening so far has been in the housing market. The pandemic-fueled housing boom of 2020 and 2021 carried over to the start of last year. Then the Federal Reserve’s effort to cool the economy and curb inflation by raising interest rates flattened housing market activity as borrowing rates more than doubled.

Existing home sales ended 2022 on a sour note, falling 1.5% month-over-month to 4.02 million units (annualized) in December – the weakest level since late 2010. Housing starts fell in December to 1.38 million (annualized) units. The housing market showed additional signs of weakness, including ongoing moderate price declines and properties spending more time on the market. Mortgage applications to purchase homes also fell from a year earlier while a measure of home-builder confidence steadily weakened in recent months.

As 2023 unfolds, new headwinds could emerge, including a softening in the labor market. This would suggest that a sustained turnaround in housing activity is unlikely to happen this year. The housing market should begin to find firmer ground in late 2023 and early 2024 – alongside an anticipated mild downtrend in mortgage rates.

Eurozone: Recent developments have hinted at some improvement in the outlook for what will still be a challenging 2023 for the Eurozone economy. A sharp drop in energy prices has driven a slowdown in headline inflation. Against this backdrop, real household incomes and consumer spending could be more resilient than previously expected and, indeed, Eurozone PMI surveys have already improved in recent months.

Many Eurozone governments have also announced fiscal measures to shield European households and businesses from higher energy prices, suggesting fiscal policy could be modestly expansionary this year. Together, lower inflation and fiscal stimulus would mean the risks are tilted towards a smaller 2023 Eurozone GDP decline than 0.6%.

Meanwhile, Eurozone policymakers have made it clear that inflation remains too high and remain concerned about the persistence of core inflation pressures. The European Central Bank's policy outlook has turned notably more hawkish since December at a time when the Fed's monetary policy outlook has started to shift in a less hawkish direction.

From a currency perspective, a more resilient Eurozone economy and a more hawkish European Central Bank could offer a more supportive mix for the euro.

China: China’s economy grew at one of its slowest rates in decades last year as repeated lockdowns hammered households and businesses, emphasizing the high cost of zero-tolerance Covid-19 policies that Beijing abruptly abandoned at the end of 2022. China's economy expanded by 3% in 2022, a sharp slowdown from the 8.1% pace recorded in 2021.

The ditching of almost all public-health restrictions in China after nearly three years of smothering even tiny virus outbreaks has set the stage for an economic rebound in 2023. A consumer-led recovery in China should occur this year to buttress global growth as the U.S. and Europe flirt with recession.

The easing of public-health restrictions has been part of a broader policy reset in China aimed at revitalizing the economy. How potent the rebound will be is still uncertain. Demand for Chinese exports has been sinking as the global economy slows. Consumer confidence has remained on the floor after three years of sporadic lockdowns. Scarring from the pandemic, in the form of vanished jobs and closed businesses, may take time to heal.

China will also face an array of longer-term challenges, including a widening confrontation with the U.S. and rapidly worsening demographics. Such a historic shift would make it harder to sustain economic growth in China without improvements in worker productivity. It should be a difficult first three months of 2023, with growth resuming in the second quarter after the worst waves of infection have receded. Emerging Market Currencies:

Emerging market currencies have outperformed over the first few weeks of 2023. This outperformance could be attributed to a Federal Reserve that has slowed the pace of monetary tightening as well as the re-opening of China's economy. The strong start for emerging market currencies should continue, although the road ahead may be a bit bumpy. As mentioned, the Fed should slow its pace of tightening, which could see U.S. yields on an overall downward trajectory over this year. As yields move lower, the depreciation pressure that has weighed on the U.S. dollar should remain intact. As the U.S. dollar depreciates, emerging market currencies should perform well and outperform relative to G10 peer currencies. However, financial markets have been currently priced for Federal Reserve rate cuts to begin around the end of this year, something Fed officials have pushed back on. Should the Fed continue to dismiss the idea of easing monetary policy this year, emerging market currencies could experience volatility and depreciation. The Fed which will eventually end its tightening cycle combined with still attractive yield opportunities in the developing world should be enough to keep capital flowing toward the emerging markets.

Outlook: The three months from October to December capped a year of economic cool-down from a rapid pandemic rebound. Last year, consumers spent at a slower pace, employers pulled back on hiring, and the housing market weakened. Despite signs of resilience, there have been concerns about the possibility of a U.S. recession this year. The Federal Reserve’s efforts to curb high inflation through rapid interest-rate increases will trigger broad spending cutbacks and job losses. The trajectory of the economy largely depends on how consumers fare in the coming months. There have been signs consumers have started to stumble. Shoppers have reined in spending on home electronics, furniture, and clothing after stocking up on those goods earlier in the pandemic. Still, inflation is coming down from historic highs at the same time wage growth has remained strong in a tight labor market. Those dynamics could help consumers’ ability and willingness to spend. Fed officials are preparing to slow interest-rate increases at their first meeting of the year and debate how much higher to raise them after gaining more confidence inflation will ease further this year. The broader economic toll from rising rates can take months to materialize, but one of the most interest-rate-sensitive sectors—housing—is showing signs of pain due to rising mortgage rates.

Sources: Department of Labor, Department of Commerce, Bloomberg, Morningstar, National Bureau of Statistics of China

Ongoing strength in the labor market has helped corroborate the view that the economy is on a positive growth path at present. Nonfarm payrolls increased by 223,000 in December. Slower inflation over the past few months, led by falling energy prices and normalizing prices for pandemic-hit sectors such as autos and airfares, has likely played a role in sustaining the momentum of the economy.

These recent developments have been encouraging signs that the U.S. economy could avoid a recession while getting inflation back to a more acceptable rate. However, the road ahead could still be challenging. The buoyancy of the labor market stands in contrast to the Institute for Supply Management’s (ISM) manufacturing and services indices, which have been pointing to a downswing in economic activity soon. The ISM indices have fallen into contractionary territory, the housing market has materially retrenched, households have taken on credit card debt and labor demand has shown signs of cooling.

U.S. consumers cut back on retail spending at the height of the holiday season spending less on vehicles, popular gifts, and furniture. Retail sales fell 1.1% in December which was the sharpest pace of 2022. This marked a dismal end to the holiday shopping season as concerns about a slowing economy pinched American consumers. Household balance sheets have not been as healthy as they were a year ago amid lower asset prices, dwindling "excess" savings, and rapidly rising credit card debt. Financial conditions have eased when viewed through the recent moves in stock prices and credit spreads, but they remained well off their all-time highs/tights, and the Treasury yield curve has still been deeply inverted across numerous maturity points.

Furthermore, core inflation has remained above the Federal Reserve's 2% inflation target, and policymakers at the Fed believe there is still work to be done on the inflation fight. As a result, monetary policy has appeared poised to become more restrictive in the months ahead, and a full pivot to rate cuts remains a long way off. The lagged effect of past policy tightening in combination with the rate hikes and balance sheet reductions still to come should impart a slowing effect on the U.S. economy as 2023 progresses.

The U.S. international trade deficit narrowed sharply to $61.5B in November, the narrowest in over two years. The narrowing was the result of a collapse in imports. While all major categories declined, the pullback in consumer goods led to the drop. While some volatile factors could explain the sharp decline, broad weakness would suggest the transition away from goods purchases by U.S. consumers may be starting to show up in import activity. While this could present some possible upside to Q4 U.S. GDP growth as the deficit falls, the details would suggest economic weakness has also started to show up in trade flows.

On balance, a recession should begin in the United States in the second half of this year, although a slightly milder one than previously expected.

On the political front, concerns about the government's ability to pay its debts resurfaced as the Treasury Department was forced to begin taking extraordinary measures to keep paying the government’s bills. By suspending certain additional investments, the Treasury would buy Congress more time – likely until June - to negotiate a resolution on how to increase the debt ceiling.

The global economy overall has shown signs of losing momentum as well. Global economic demand weakened toward the end of 2022 under the weight of high inflation and rising interest rates, combined with challenges caused by the war in Ukraine and Covid-19 lockdowns in China.

Inflation: U.S. inflation eased in December for the sixth straight month as the Federal Reserve aggressively raised interest rates and the economy showed signs of cooling. The consumer-price index rose 6.5% in December from a year earlier, down from 7.1% in November and well below a 9.1% peak in June.

Core CPI climbed 5.7% in December from a year earlier, easing from a 6% gain in November. Core prices increased at a 3.1% annualized rate in the three months that ended in December, the slowest pace in more than a year and down from 7.9% in June.

These figures added to signs that inflation has turned a corner following last year’s surge. Goods prices, a key driver of inflation over the past year and a half, fell for the third straight month in December. Improving supply chains and reduced demand have relieved price pressures on goods, but service prices continued to climb in part because of wage gains in a tight labor market. High wage growth could keep consumers flush with cash and companies eager to raise prices to compensate, holding inflation above the Fed’s 2% target. Taming services inflation will be the Fed’s biggest challenge this year.

Labor market: Employers added 4.5 million jobs in 2022 showing that the labor market remained a source of U.S. economic strength at a time of high inflation, climbing interest rates, and uneven growth. The U.S. economy added 223,000 jobs in December. The unemployment rate ticked lower to 3.5% – returning to its 50-year low. The participation rate edged higher rising to 62.3% and ending the year about where it started. Average hourly earnings rose 0.3% month-over-month (m/m) – a deceleration from the 0.4% m/m gain recorded in November. Compared to December 2021, wage growth was up 4.6%. The continuing effects of the economy’s bounce back following Covid-19 lockdowns, a wave of retirements early in the pandemic, and strong household spending have pushed up employer demand for workers—and paychecks—when those workers have been scarce. Wage growth has been identified by the Federal Reserve as the primary source fueling higher inflation across many of the labor-intensive service sectors.

Hiring had been resilient throughout 2022 despite an economy that has slowed alongside the Federal Reserve’s aggressive pace of interest rate increases aimed at bringing down inflation. However, some recent data and a wave of tech and finance industry layoffs have suggested the labor market, while still vibrant, may be starting to lose momentum and gains could reverse in the year ahead.

But there are still 1.7 job openings for every person actively looking for work. With labor force growth showing little improvement this past year, labor demand will need to slow considerably more to restore balance in the labor market and cool wage pressures.

This year could be more challenging for the labor market as the economy absorbs the impact of slowing global growth and the lagged effect of higher interest rates.

Housing: The clearest impact of Fed tightening so far has been in the housing market. The pandemic-fueled housing boom of 2020 and 2021 carried over to the start of last year. Then the Federal Reserve’s effort to cool the economy and curb inflation by raising interest rates flattened housing market activity as borrowing rates more than doubled.

Existing home sales ended 2022 on a sour note, falling 1.5% month-over-month to 4.02 million units (annualized) in December – the weakest level since late 2010. Housing starts fell in December to 1.38 million (annualized) units. The housing market showed additional signs of weakness, including ongoing moderate price declines and properties spending more time on the market. Mortgage applications to purchase homes also fell from a year earlier while a measure of home-builder confidence steadily weakened in recent months.

As 2023 unfolds, new headwinds could emerge, including a softening in the labor market. This would suggest that a sustained turnaround in housing activity is unlikely to happen this year. The housing market should begin to find firmer ground in late 2023 and early 2024 – alongside an anticipated mild downtrend in mortgage rates.

Eurozone: Recent developments have hinted at some improvement in the outlook for what will still be a challenging 2023 for the Eurozone economy. A sharp drop in energy prices has driven a slowdown in headline inflation. Against this backdrop, real household incomes and consumer spending could be more resilient than previously expected and, indeed, Eurozone PMI surveys have already improved in recent months.

Many Eurozone governments have also announced fiscal measures to shield European households and businesses from higher energy prices, suggesting fiscal policy could be modestly expansionary this year. Together, lower inflation and fiscal stimulus would mean the risks are tilted towards a smaller 2023 Eurozone GDP decline than 0.6%.

Meanwhile, Eurozone policymakers have made it clear that inflation remains too high and remain concerned about the persistence of core inflation pressures. The European Central Bank's policy outlook has turned notably more hawkish since December at a time when the Fed's monetary policy outlook has started to shift in a less hawkish direction.

From a currency perspective, a more resilient Eurozone economy and a more hawkish European Central Bank could offer a more supportive mix for the euro.

China: China’s economy grew at one of its slowest rates in decades last year as repeated lockdowns hammered households and businesses, emphasizing the high cost of zero-tolerance Covid-19 policies that Beijing abruptly abandoned at the end of 2022. China's economy expanded by 3% in 2022, a sharp slowdown from the 8.1% pace recorded in 2021.

The ditching of almost all public-health restrictions in China after nearly three years of smothering even tiny virus outbreaks has set the stage for an economic rebound in 2023. A consumer-led recovery in China should occur this year to buttress global growth as the U.S. and Europe flirt with recession.

The easing of public-health restrictions has been part of a broader policy reset in China aimed at revitalizing the economy. How potent the rebound will be is still uncertain. Demand for Chinese exports has been sinking as the global economy slows. Consumer confidence has remained on the floor after three years of sporadic lockdowns. Scarring from the pandemic, in the form of vanished jobs and closed businesses, may take time to heal.

China will also face an array of longer-term challenges, including a widening confrontation with the U.S. and rapidly worsening demographics. Such a historic shift would make it harder to sustain economic growth in China without improvements in worker productivity. It should be a difficult first three months of 2023, with growth resuming in the second quarter after the worst waves of infection have receded. Emerging Market Currencies:

Emerging market currencies have outperformed over the first few weeks of 2023. This outperformance could be attributed to a Federal Reserve that has slowed the pace of monetary tightening as well as the re-opening of China's economy. The strong start for emerging market currencies should continue, although the road ahead may be a bit bumpy. As mentioned, the Fed should slow its pace of tightening, which could see U.S. yields on an overall downward trajectory over this year. As yields move lower, the depreciation pressure that has weighed on the U.S. dollar should remain intact. As the U.S. dollar depreciates, emerging market currencies should perform well and outperform relative to G10 peer currencies. However, financial markets have been currently priced for Federal Reserve rate cuts to begin around the end of this year, something Fed officials have pushed back on. Should the Fed continue to dismiss the idea of easing monetary policy this year, emerging market currencies could experience volatility and depreciation. The Fed which will eventually end its tightening cycle combined with still attractive yield opportunities in the developing world should be enough to keep capital flowing toward the emerging markets.

Outlook: The three months from October to December capped a year of economic cool-down from a rapid pandemic rebound. Last year, consumers spent at a slower pace, employers pulled back on hiring, and the housing market weakened. Despite signs of resilience, there have been concerns about the possibility of a U.S. recession this year. The Federal Reserve’s efforts to curb high inflation through rapid interest-rate increases will trigger broad spending cutbacks and job losses. The trajectory of the economy largely depends on how consumers fare in the coming months. There have been signs consumers have started to stumble. Shoppers have reined in spending on home electronics, furniture, and clothing after stocking up on those goods earlier in the pandemic. Still, inflation is coming down from historic highs at the same time wage growth has remained strong in a tight labor market. Those dynamics could help consumers’ ability and willingness to spend. Fed officials are preparing to slow interest-rate increases at their first meeting of the year and debate how much higher to raise them after gaining more confidence inflation will ease further this year. The broader economic toll from rising rates can take months to materialize, but one of the most interest-rate-sensitive sectors—housing—is showing signs of pain due to rising mortgage rates.

Sources: Department of Labor, Department of Commerce, Bloomberg, Morningstar, National Bureau of Statistics of China

Disclosures:

Past performance quoted is past performance and is not a guarantee of future results. Portfolio diversification does not guarantee investment returns and does not eliminate the risk of loss. The opinions and estimates put forth constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Securities are not insured by FDIC or any other government agency, are not bank guaranteed, are not deposits or a condition to any banking service or activity, are subject to risk and may lose value, including the possible loss of principal.

Atlantic Union Bank Wealth Management is a division of Atlantic Union Bank that offers asset management, private banking, and trust and estate services. Securities are not insured by the FDIC or any other government agency, are not deposits or obligations of Atlantic Union Bank, are not guaranteed by Atlantic Union Bank or any of its affiliates, and are subject to risks, including the possible loss of principal. Deposit products are provided by Atlantic Union Bank, Member FDIC.