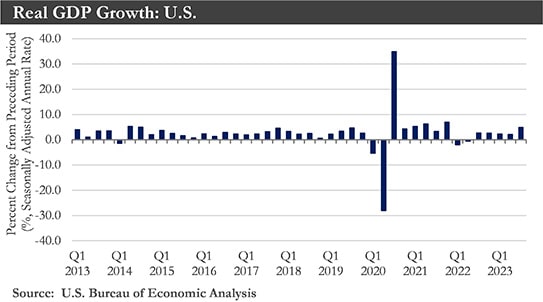

Recap: U.S. economic activity remained strong in 2023 as the economy withstood the initial shock associated with the rapid pace of monetary tightening. The final reading on U.S. GDP showed that the economy grew by 4.9% (annualized) in the third quarter, a downgrade of 0.3 percentage points from the second estimate in November.

A surprise increase in November retail sales dispelled lingering pessimism about the economy and reinforced growing sentiment that the U.S. could beat inflation without paying the price in significantly weaker growth. Also in November, the unemployment rate fell, inflation cooled, and the Federal Reserve pivoted away from raising interest rates while considering when to cut them. With inflation still too high and the FOMC committed to bringing it down to 2%, it did not fully close the door to additional policy tightening. While further tightening has remained possible, it has grown less probable.

The resilient labor market that supported an unexpectedly strong U.S. economy last year has shown signs of cooling. Continuing jobless claims rose to 1.93 million in mid-November, the highest level since late 2021 and an added sign that the labor market has been cooling.

On the production side, the services sector of the economy managed to expand with the ISM services index rising modestly to 52.7 in November. This lackluster growth suggests that activity in the sector has slowed, which should help to keep a lid on service sector inflation and should help wage inflation cool further.

Overall, consumer spending probably remained buoyant over the holiday period, but the momentum may be fading, with consumption growth likely to slow in the coming quarter.

The pullback in mortgage rates appeared to have provided some relief for housing, with mortgage purchase applications ticking higher for more than a month. But, the impact of interest rates has a lag, so this could take some time to be manifested in sales activity. To that end, pending home sales fell to an all-time low in November, indicating that things would get worse before they get better.

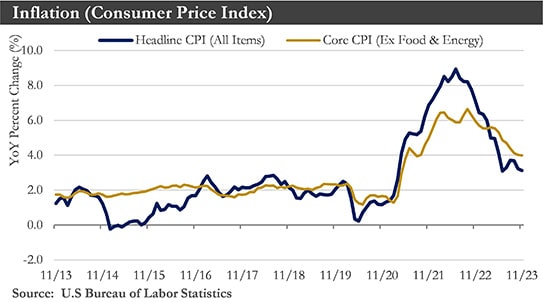

Inflation eased considerably in 2023 amid tight monetary policy, standing at 3.1% in November. Outright declines in energy prices have put the biggest dent in inflation over the past year, but price growth has slowed for other major categories, including food, core goods, housing, and core services.

Smoother functioning supply chains, and restrained consumer spending have helped slow price increases for goods. Lower goods prices could ease inflation’s path down towards the Fed’s target. Prices for services have cooled though demand has persisted. Shelter costs are one factor that could help further slow inflation in coming months.

U.S. Outlook for 2024: Prospects for economic growth are shifting as the economy progresses into 2024. Conditions are tracking toward a below-trend pace of activity amid growing macroeconomic vulnerabilities and increasingly tight financial conditions. Although it is likely the Federal Reserve’s tightening cycle has come to an end, the slow return to 2% inflation suggests the Fed’s Open Market Committee (FOMC) is still a long way from easing policy.

While the U.S. economy has withstood higher interest rates, some cracks have begun to emerge. This weakness has been most evident in the residential investment sector, where elevated mortgage rates combined with low levels of existing home inventory for sale have crimped affordability and weighed on sales. Sales activity is likely to remain under pressure in 2024 as rates remain elevated.

Businesses have also pared back new capital expenditures amid increased economic uncertainty and a generally less favorable spending environment. Higher borrowing costs have made it less affordable for businesses to borrow and invest, which has deterred new activity. Many businesses could experience higher interest expenses, which would further weigh on their ability to make new capital investments and expand payrolls.

Consumer spending has been one of the most resilient sectors of overall spending in 2023, but the drivers of household purchasing power have shifted. The ability of households to easily rely on their balance sheets to spend in 2024 has faded. Excess liquidity has dried up and become concentrated among higher-income households that have a lower propensity to spend. Access to credit has also weakened as banks have become more cautious in making new loan commitments to consumers, portending a pullback in overall revolving credit. In short, the financial position of the household sector has remained in decent shape but could deteriorate at the margin.

Additional progress in reducing inflation has been dependent on the trajectory of the labor market. While inflation should recede further, additional progress is likely to prove slower going than it has over the past year. Disinflation from a normalizing supply chain constraints has nearly run its course, and it is only a matter of time before housing disinflation more materially takes hold and follows the moderation in home and rental prices. The rise in labor costs has run too high to be consistent with 2% consumer price inflation, but further labor market moderation should lead to a gradual downdraft in core inflation as well.

The probability of a soft landing, where growth slows but contraction is circumvented, would be significant. But even in the event the economy avoids a recession, growth in 2024 should be subpar, at best, due to the elevated level of real interest rates. Labor market prospects have dimmed, and consumer spending momentum has begun to fade. Lower interest rates should occur in 2024, unless inflation stops retreating.

Real GDP growth could slow materially heading into 2024 and a modest contraction in economic activity could take hold by the second quarter. Economic weakness, which has helped push inflation back toward the Fed's target of 2% on a sustained basis, should then induce the FOMC to begin easing monetary policy. Even as the Fed eases policy next year, rates are likely to settle at a higher level than what prevailed ahead of the pandemic.

U.S. Dollar in 2024: After an extended period of U.S. dollar strength in 2022, it was a back-and-forth year for the dollar in 2023. Given a still uncertain backdrop heading into 2024, the U.S. dollar should remain a safe place to be for at least the next several months. U.S dollar appreciation through at least Q1-2024 and longer is a real possibility. This outlook for further U.S. dollar gains has stemmed from the ongoing resilience in U.S. activity and improving prospects for a softer landing, which has left open the possibility of a further Fed hike. U.S. dollar strength could be particularly noticeable against the euro and British pound, where sharply slower growth along with central banks that have probably reached the end of their tightening cycles would be factors likely to weigh on those currencies.

The trend of U.S. dollar strength should eventually slow down and turn to U.S. dollar weakness later in 2024, caused by a mild U.S. slow down, and easing monetary policy from the Fed.

Global Economy in 2024: The global economy could face an unsettled climate in 2024 and, indeed, the economic storm could be quite severe at certain times and for certain economies. To be sure, the global growth outlook has already been clouded for a while. After global growth of 3.5% in 2022, the global economy grew more slowly in 2023 with further deceleration expected in 2024.

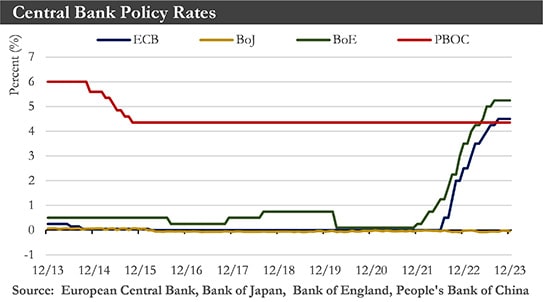

The most important factor behind the ongoing slowdown in the pace of global expansion has been the continued impact of aggressive monetary tightening by most of the world's central banks over the past couple of years. The long and variable lags between changes in monetary policy and their impact on economic growth and inflation has meant the effects of restrictive monetary policy will likely continue to be felt for several quarters ahead. However, that influence could be felt differently across major economies. The decline in global inflation already under way should continue in 2024.

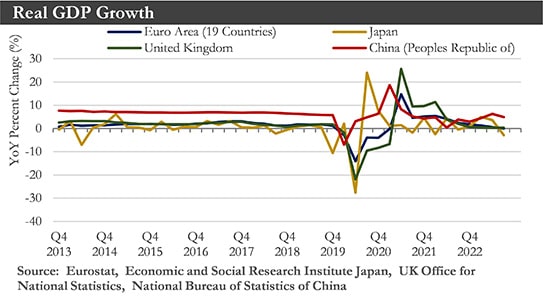

The 2024 economic storm clouds should have a differing impact across major economies, with some countries likely to experience a more pronounced growth slowdown than others through late 2023 and into 2024. Among the hardest hit would be the economies of the Eurozone. Economic momentum across Europe has already slowed sharply and Purchasing Manager surveys have fallen to levels that have historically been consistent with a contracting economy. However, real household income trends have held up reasonably well, and interest costs across the Eurozone have risen. Meanwhile, although Eurozone corporate profit growth has slowed, profits have so far not experienced any significant decline. With Eurozone real household income trends improving and corporate profits stable so far, these dynamics could help the region narrowly avoid recession. That said, Eurozone GDP growth has been forecast to be just 0.5% for all of 2023 and below 1% for 2024.

The burst of activity seen in early 2023 in China after the economy reopened post-COVID proved to be relatively short-lived. Economic momentum has slowed noticeably in 2023, especially in consumer, services, and real estate sectors. In response, authorities have delivered a range of measures over the past several months aimed at cushioning this economic slowdown. These measures have led to a brief and modest improvement in activity, as Q3 GDP grew more than expected, and economic activity data has firmed in recent months. Against this backdrop, 2023 Chinese GDP growth forecast should be about 5.0%. That said, China's economy should continue to face structural headwinds to growth. Real estate sector problems, demographic challenges, sluggish consumption trends, and geopolitical tensions all likely will place downward pressure on growth prospects over the medium to longer term. Slower growth is expected in 2024.

Outlook: Prospects for economic growth in the U.S. are shifting as the economy progresses into 2024. Real GDP growth will likely slow materially heading into 2024 and a modest contraction in economic activity could well take hold by the second quarter. Economic weakness, which will help push inflation back toward the Fed's target of 2% on a sustained basis, should then induce the FOMC to begin easing monetary policy. Even as the FOMC eases policy later this year, interest rates will likely settle at a higher level than what prevailed ahead of the pandemic.

The U.S. dollar and U.S. dollar-based assets will remain a safe place to be for now. The trend of U.S. dollar strength will likely slow and turn to U.S. dollar weakness later in 2024.

The global economy is likely to experience a period of below-trend growth in 2024, with the global economy expanding at just about 2.5%. Growth prospects should be restrained by a U.S. economy potentially experiencing a mild recession in mid-2024, recessions in the Eurozone and U.K., as well as a Chinese economy decelerating amid structural challenges. Some economies could outperform and grow at above-trend rates. Asia, in particular India, should be the region and economy that stands out from a growth perspective.

Sources: Department of Labor, Department of Commerce, Institute for Supply Management, Bloomberg, People’s Bank of China, European Commission, European Central Bank

Capital Market Commentary

Recap: Stock markets across the globe posted spectacular December returns which added to the substantial gains achieved through the first 11 months of the year. And bond markets too posted solid gains last month providing investors a healthy return for the full year after a difficult 2022. Markets seem to have responded to the surprising resilience of the U.S. economy and its labor market despite the headwinds of still elevated inflation and high interest rates. The Federal Reserve’s signal that the end of their rate hiking campaign had probably arrived gave markets reason to celebrate./p>

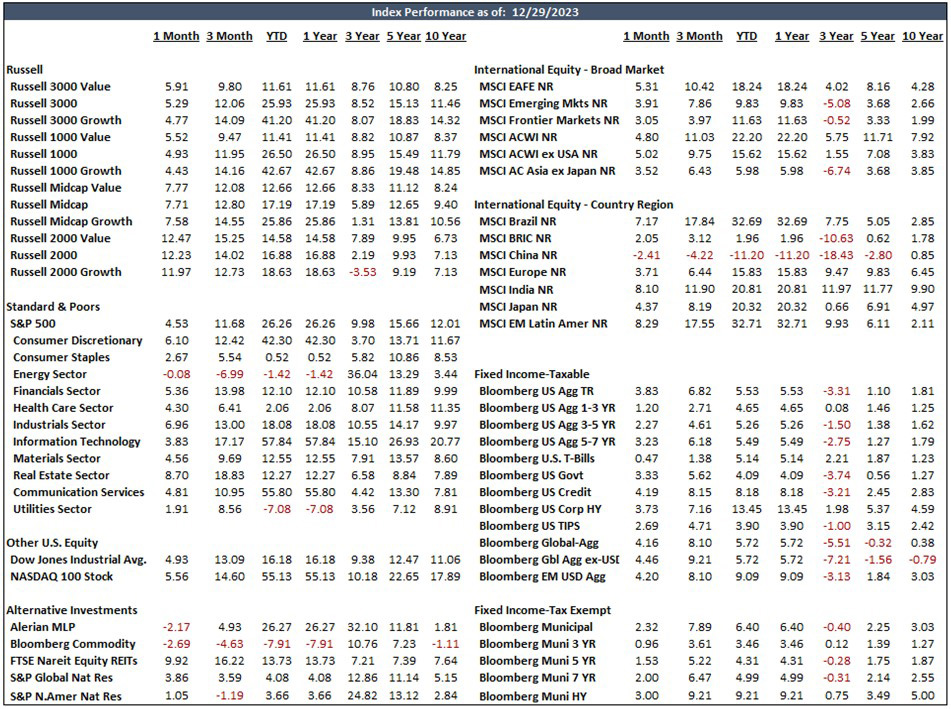

U.S. stocks across the capitalization and style spectrum delivered robust gains in the fourth quarter. Virtually every capitalization and style type posted double digits gains for the quarter. In a return to recent form, growth style stocks handily outpaced value stocks while in a reversal of fortune, small-cap and mid-cap stocks outpaced large cap stocks. The S&P 500 was up 11.7%, the Russell Mid Cap Index was up 12.8%, while Small Cap stocks were up 14.1% in Q4. For the full year, the S&P 500 was 26.3%, while Mid Cap and Small Cap were up 17.2% and 16.8% respectively. All, truly outstanding returns that are well above historical norms.

Bonds too got in on the party! The broad Bloomberg Aggregate posted a 6.8% return for the fourth quarter and a 5.5% return for the full year. With signals that the Federal Reserve is likely done hiking rates and their next move was likely a rate cut, long-dated bonds outpaced shorter term maturities. And not surprisingly, bonds with higher credit risk than U.S. Treasuries posted the highest returns with corporate bonds up 8.2% for the quarter while junk bonds were up 7.2% and the Bloomberg Global Aggregate Bond Index ex-U.S. bonds was up 9.2%.

Outlook: The outlook for stock returns in the near term, despite the strong returns of 2023, remains uncertain given the slowly deteriorating dynamics of the economy, still relatively high interest rates, a Federal Reserve resolute in its battle to fight inflation, and what are historically expensive stock prices. This is especially true for the handful of market leading growth stocks referred to as the “Magnificent Seven” (i.e., Alphabet, Amazon, Apple, Meta, Microsoft, Tesla, and NVIDIA). This mix of headwinds will likely continue to weigh on corporate profit growth for some time. The equity markets however seem to have priced in a near certain soft economic landing, with lower interest rates, and reaccelerating corporate profit growth for 2024.

The outlook for bonds continues to look pretty bright, mainly due to the likelihood that the Fed is closer to the end of its rate hiking cycle, inflation is coming down, and now bonds offer a respectable coupon rate after years of ultra-low interest rates. Bond coupon rates finally provide real competition for investment dollars versus stocks for more conservative income-oriented investors, given the more expensive investment profile of stocks in general.

There continue to be downside risks to the capital markets, which should be kept in mind as 2024 unfolds. Those risks include gridlock in a hyper partisan Congress over important issues like the federal budget, immigration, and funding conflicts in Europe and the Middle East. The latter is already impacting trade as ships with cargo are forced to take longer more expensive routes around the southern tip of Africa to avoid blockades and conflicts near the Suez Canal. And we should not forget the races for the Presidency and Congressional seats that are now heating up. Presidential years tend to be positive years for equity returns (though past performance is no guarantee of future results).

Also, historically the Federal Reserve tends to avoid changing their monetary policy in any meaningful way as elections approach so as not to appear partisan. And finally, if forces that could negatively impact inflation (like the price of oil, or commodities, or increased demand for goods and services) slow the decline of inflation or even reverse it, it would be unlikely the Fed would cut rates as much as markets are expecting. Any combination of the above risks could disappoint investors.

The longer-term view of markets suggests that the tailwinds stock and bond investors enjoyed in recent years, including massive fiscal stimulus and declining and ultra-low interest rates, will not resurface soon to smooth over inevitable hard economic times. Securities’ values are more likely to be driven by the organic operational successes of businesses rather than help from the federal government. These conditions should favor astute stock and bond selection.

Disclosures:

Past performance quoted is past performance and is not a guarantee of future results. Portfolio diversification does not guarantee investment returns and does not eliminate the risk of loss. The opinions and estimates put forth constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. Securities are not insured by FDIC or any other government agency, are not bank guaranteed, are not deposits or a condition to any banking service or activity, are subject to risk and may lose value, including the possible loss of principal.

Atlantic Union Bank Wealth Management is a division of Atlantic Union Bank that offers asset management, wealth banking, and trust and estate services. Securities are not insured by the FDIC or any other government agency, are not deposits or obligations of Atlantic Union Bank, are not guaranteed by Atlantic Union Bank or any of its affiliates, and are subject to risks, including the possible loss of principal. Deposit products are provided by Atlantic Union Bank, Member FDIC