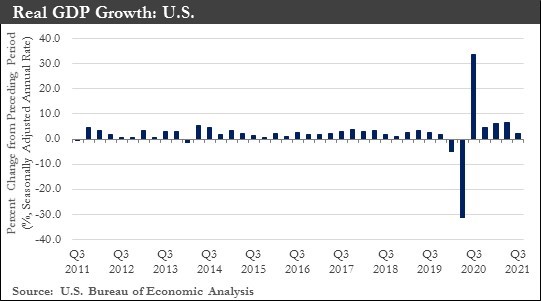

Recap: The U.S. economy grew by 2.0% in the third quarter of 2021, with the Delta variant of Covid-19 and supply issues dampening gains. Such a pace marked a sharp slowdown from robust gains earlier this year. GDP grew at a historically fast annual rate of 6.3% in the first quarter and 6.7% in the second quarter as an infusion of government stimulus, widespread business reopening, and rising vaccination rates all fueled spending.

Those spending drivers faded from July to September. Two additional factors arose over the summer to dampen third-quarter growth: surging in virus cases and deepening supply bottlenecks.

Fortunately, the Delta variant has become less disruptive in the U.S. with case counts falling and vaccinations rising. As one problem fades, another has gotten worse. Supply chain issues had been prominent to varying degrees since the pandemic first broke out in March 2020, but in recent months, supply chains have shifted from merely a major headache to an outright crisis.

COVID case spiked overseas and the resulting absenteeism at far-flung ports and factories have had a lagged effect on the production pipeline all over the world. The result has been the “everything shortage.” The logjam could push back the timing of some growth anticipated later this year and early next year, which would weigh on the forecast for 2022.

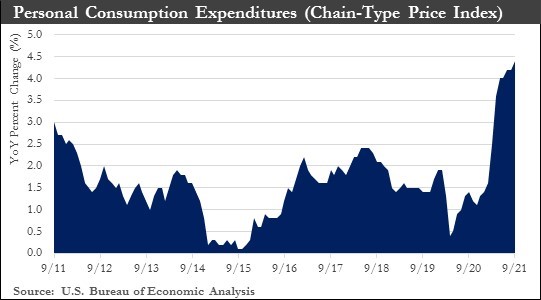

The shortages and longer wait times have affected consumer prices. Headline inflation, as measured by the PCE deflator, rose to 4.3% on a year-over-year basis, with core PCE deflator coming in at 3.6%. These measures have reflected the highest headline and core inflation in more than 30 years. The FOMC could announce tapering its asset purchases later this year, which should contribute to the upward creep in long-term interest rates forecast for the coming quarters.

The supply chain crisis may drive prices even higher and slow economic growth, but because household and business balance sheets have generally been in solid shape, the economic expansion should remain intact, even if somewhat held back by these headwinds. Real GDP is forecasted to grow 4.0% in 2022.

Congress has passed an 11th-hour deal to keep the government funded through December, averting a shutdown. The extension of the debt ceiling to early December would remove the most ominous storm cloud hanging over the economy and may set the table for stronger gains in coming months. Congress has gone through many of these brinksmanship debacles over the years, but it has never failed to make its debt payments. A deal should be reached, but likely at the last minute.

Labor Market: The labor market recovery has continued to be held back by the availability of labor. Demand indicators have continued to hover near record levels, including job openings, small business hiring plans, and consumers' views that jobs are "plentiful." Yet workers have remained slow to return to the labor market. Despite schools opening, emergency unemployment benefits ending and the latest wave of COVID peaking, the labor force participation rate has slipped in recent months. With labor supply, rather than demand, being the biggest challenge to hiring right now, the jobs market has continued to tighten. The unemployment rate tumbled to 4.8% in September. Wage pressures over the next few quarters should be stronger as a result. However, constraints on the labor supply could ease in the coming months, which should support somewhat stronger hiring early next year and keep wages from spiraling higher.

Inflation: Consumer prices have risen at the fastest rate this year in more than a decade. The inflation surge has been driven by a combination of economic forces. The rebound in consumer demand has come much sooner and much stronger than usual in the aftermath of an economic contraction, but supply has struggled to meet that demand. Expecting a more subdued and more drawn-out recovery, few manufacturers have added capacity during the Covid-19 pandemic, while factories and many parts of the global transport network have been hindered by government restrictions on work and movement.

Although the latest readings on inflation have supported the view that the most acute price hikes have passed, inflation would not fade quietly. Energy prices have been back on the advance, with oil and natural gas prices near seven-year highs. Meanwhile, supply chain bottlenecks have continued to plague the goods sector and could likely persist well into next year.

The near-term outlook for inflation has risen as result. PCE inflation should peak in the first quarter, with core PCE inflation hitting 4.4%. As spending shifts back toward services and income growth slows, easing demand for goods and fewer COVID-related supply disruptions next year should help goods inflation come off the boil. Yet inflation would remain elevated as the tightening labor market keeps wage growth strong and housing inflation picks up. PCE inflation could run around 2.0% in 2023 as structural forces that held down inflation in the past exert as much downward pressure on inflation in the years ahead.

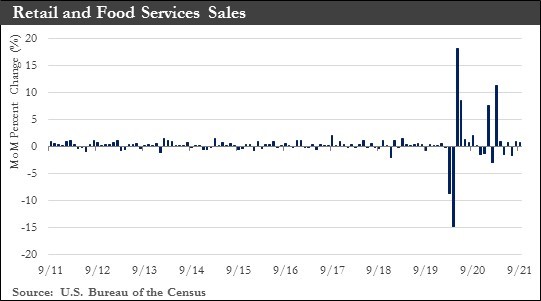

Retail Sales: American consumers have stepped up their spending in September, a sign of resilient demand and rising inflation. September retail sales rose a seasonally adjusted 0.7% from the previous month as households shrugged off supply constraints, the Delta variant, and the end of enhanced unemployment benefits.

There have been a couple of forces weighing on future retail sales. First, services spending has significant pent-up demand, and consumers have shifted spending towards services and away from retail goods. Second, supply constraints, most notably for motor vehicles, but also other tradable goods, have prevented people from making purchases. The latter was evident in falling vehicle sales in September. The first would be a force restrained spending on goods over the medium term and why very little growth in durables spending could occur in the coming months.

Federal Reserve: With the economy growing at an above-trend rate and the labor market continuing to heal, the Federal Open Market Committee (FOMC) will eventually take its foot off the monetary policy accelerator. The Fed currently has purchased $80 billion of Treasury securities and $40 billion of mortgage-backed securities (MBS) per month. The FOMC could announce that it will begin to taper its asset purchases soon. Although the exact pace of tapering is still unclear, policymakers will set the pace such that purchases cease by mid-2022, which should contribute to the upward rise in long-term interest rates. However, actual interest rate hikes by the Federal Reserve could still be some ways off.

Global Supply Chain: Global supply-chain bottlenecks have been feeding on one another, with shortages of components and surging prices of critical raw materials squeezing manufacturers around the world. The supply shocks have already shown signs of choking off the recovery in some regions.

Part of the problem has been a global economy that is out of sync on the pandemic, restrictions, and recovery. Factories and retailers in Western economies that have largely emerged from lockdowns are eager for finished products, raw materials, and components from longtime suppliers in Asia and elsewhere. But many countries in Asia have still been in the throes of lockdowns and other coronavirus-related restrictions, constricting their ability to meet demand.

Meanwhile, global labor shortages, often the result of people leaving the workforce during the pandemic, have thrown further obstacles in the way of producers. The bottlenecks will constrain manufacturing output well into next year, hurting a sector that had until recently powered the global recovery.

Supply-chain disruptions have helped push inflation to multidecade highs in the U.S. and parts of Europe, weighing on consumer spending. Supply constraints for manufacturers are squeezing margins and pushing up consumer prices. Elevated inflation rates have already put pressure on central banks, including the Federal Reserve, to start scaling back their aggressive pandemic stimulus policies, a further headwind to global growth.

Global: The global economy has continued to face a flurry of issues. COVID-related growth disruptions have been persistent, while regulatory changes and property sector challenges have weighed on China's economy. Europe has handled the wave of the highly infectious Delta-variant well, outperforming expectations in the first half of the year. In contrast, emerging markets (EM) with insufficient vaccine access and healthcare infrastructures have been devastated by its effects. The COVID threat to the EM economies will persist in the near term. Against this backdrop, the outlook for the global economy has softened, and risks around the global growth forecast have remained tilted to the downside. Global growth is expected to be around 5.8% in 2021.

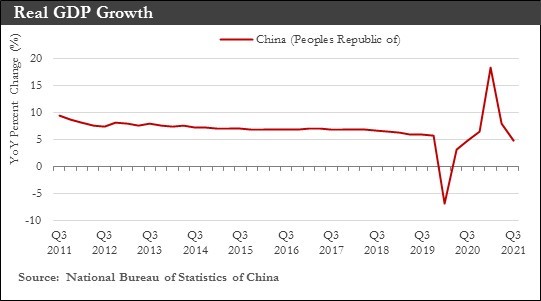

China: China's economy has slowed in recent months, as COVID-related restrictions have weighed on services and retail activity in particular while regulatory changes and real estate disruptions have more recently held back activity.

China's economy has experienced an increase in leverage over the past decade including, importantly, an increase in corporate leverage. While a corporate debt crisis in China has not materialized to date, recent developments related to Evergrande, one of China's largest property developers, suggested the likelihood has risen. At the same time, regulatory changes have escalated Evergrande's default risk. A default or disorderly collapse of Evergrande would have negative implications for China's real estate industry and for the broader Chinese economy. Furthermore, it is possible that Evergrande's financial problems may not be isolated, as China's system-wide leverage—including its non-financial corporate debt levels—have been quite elevated.

That said, Chinese elevated corporate debt has been a vulnerability to China's economy and a moderate risk to the global economy, but not likely a problem that will cause the next Global Financial Crisis a-la 2008. A collapse in China's real estate market, were it to occur, is not expected to prompt another Lehman Brothers moment. This has been, in part, because China's foreign debt exposure is currently much lower than what the U.S. foreign debt exposures were before the 2008 Global Financial Crisis.

Outlook: The downward adjustment to the U.S. outlook does not negate a solid rebound of 5.5% for 2021. Looking ahead to 2022, growth is expected to follow through at a solid 4.0% rate as more activities normalize while the pandemic recedes. Continued above-trend growth in 2023 is expected to drive the unemployment rate slightly below its pre-pandemic low to 3.4% enabling rate hikes by the Federal Reserve.

Downside risks stem from the ongoing uncertainty of the virus and variants, along with the possibility that supply-side constraints could weigh more heavily on production and consumption. On the upside, Americans have built up a substantial cash cushion, which could drive spending higher than we assume. Fiscal policy presents both upside and downside risks. It is assumed that Congress passes the Infrastructure Investment and Jobs Act. Any misstep here would therefore present a modest disappointment. On the other hand, Democrats have even larger plans for social spending, funded by tax increases. This could present a boost to growth next year depending on the final details. The Federal Reserve will likely maintain the current low-rate environment until the final quarter of 2022. At that point, it is expected to initiate rate hiking cycles, with the federal funds rate reaching 2.0% by 2024.

Over the coming quarters, government yields are likely to continue to rise. This rise will be driven by three factors: first, markets will continue to solidify a higher policy path for the federal funds rate; second, the Federal Reserve will end net-new bond purchases over the coming quarters; and third, lingering inflation will cause investors to demand higher compensation for inflation risk.

This Newsletter was produced for Atlantic Union Bank Wealth Management by Capital Market Consultants, Inc.

Those spending drivers faded from July to September. Two additional factors arose over the summer to dampen third-quarter growth: surging in virus cases and deepening supply bottlenecks.

Fortunately, the Delta variant has become less disruptive in the U.S. with case counts falling and vaccinations rising. As one problem fades, another has gotten worse. Supply chain issues had been prominent to varying degrees since the pandemic first broke out in March 2020, but in recent months, supply chains have shifted from merely a major headache to an outright crisis.

COVID case spiked overseas and the resulting absenteeism at far-flung ports and factories have had a lagged effect on the production pipeline all over the world. The result has been the “everything shortage.” The logjam could push back the timing of some growth anticipated later this year and early next year, which would weigh on the forecast for 2022.

The shortages and longer wait times have affected consumer prices. Headline inflation, as measured by the PCE deflator, rose to 4.3% on a year-over-year basis, with core PCE deflator coming in at 3.6%. These measures have reflected the highest headline and core inflation in more than 30 years. The FOMC could announce tapering its asset purchases later this year, which should contribute to the upward creep in long-term interest rates forecast for the coming quarters.

The supply chain crisis may drive prices even higher and slow economic growth, but because household and business balance sheets have generally been in solid shape, the economic expansion should remain intact, even if somewhat held back by these headwinds. Real GDP is forecasted to grow 4.0% in 2022.

Congress has passed an 11th-hour deal to keep the government funded through December, averting a shutdown. The extension of the debt ceiling to early December would remove the most ominous storm cloud hanging over the economy and may set the table for stronger gains in coming months. Congress has gone through many of these brinksmanship debacles over the years, but it has never failed to make its debt payments. A deal should be reached, but likely at the last minute.

Labor Market: The labor market recovery has continued to be held back by the availability of labor. Demand indicators have continued to hover near record levels, including job openings, small business hiring plans, and consumers' views that jobs are "plentiful." Yet workers have remained slow to return to the labor market. Despite schools opening, emergency unemployment benefits ending and the latest wave of COVID peaking, the labor force participation rate has slipped in recent months. With labor supply, rather than demand, being the biggest challenge to hiring right now, the jobs market has continued to tighten. The unemployment rate tumbled to 4.8% in September. Wage pressures over the next few quarters should be stronger as a result. However, constraints on the labor supply could ease in the coming months, which should support somewhat stronger hiring early next year and keep wages from spiraling higher.

Inflation: Consumer prices have risen at the fastest rate this year in more than a decade. The inflation surge has been driven by a combination of economic forces. The rebound in consumer demand has come much sooner and much stronger than usual in the aftermath of an economic contraction, but supply has struggled to meet that demand. Expecting a more subdued and more drawn-out recovery, few manufacturers have added capacity during the Covid-19 pandemic, while factories and many parts of the global transport network have been hindered by government restrictions on work and movement.

Although the latest readings on inflation have supported the view that the most acute price hikes have passed, inflation would not fade quietly. Energy prices have been back on the advance, with oil and natural gas prices near seven-year highs. Meanwhile, supply chain bottlenecks have continued to plague the goods sector and could likely persist well into next year.

The near-term outlook for inflation has risen as result. PCE inflation should peak in the first quarter, with core PCE inflation hitting 4.4%. As spending shifts back toward services and income growth slows, easing demand for goods and fewer COVID-related supply disruptions next year should help goods inflation come off the boil. Yet inflation would remain elevated as the tightening labor market keeps wage growth strong and housing inflation picks up. PCE inflation could run around 2.0% in 2023 as structural forces that held down inflation in the past exert as much downward pressure on inflation in the years ahead.

Retail Sales: American consumers have stepped up their spending in September, a sign of resilient demand and rising inflation. September retail sales rose a seasonally adjusted 0.7% from the previous month as households shrugged off supply constraints, the Delta variant, and the end of enhanced unemployment benefits.

There have been a couple of forces weighing on future retail sales. First, services spending has significant pent-up demand, and consumers have shifted spending towards services and away from retail goods. Second, supply constraints, most notably for motor vehicles, but also other tradable goods, have prevented people from making purchases. The latter was evident in falling vehicle sales in September. The first would be a force restrained spending on goods over the medium term and why very little growth in durables spending could occur in the coming months.

Federal Reserve: With the economy growing at an above-trend rate and the labor market continuing to heal, the Federal Open Market Committee (FOMC) will eventually take its foot off the monetary policy accelerator. The Fed currently has purchased $80 billion of Treasury securities and $40 billion of mortgage-backed securities (MBS) per month. The FOMC could announce that it will begin to taper its asset purchases soon. Although the exact pace of tapering is still unclear, policymakers will set the pace such that purchases cease by mid-2022, which should contribute to the upward rise in long-term interest rates. However, actual interest rate hikes by the Federal Reserve could still be some ways off.

Global Supply Chain: Global supply-chain bottlenecks have been feeding on one another, with shortages of components and surging prices of critical raw materials squeezing manufacturers around the world. The supply shocks have already shown signs of choking off the recovery in some regions.

Part of the problem has been a global economy that is out of sync on the pandemic, restrictions, and recovery. Factories and retailers in Western economies that have largely emerged from lockdowns are eager for finished products, raw materials, and components from longtime suppliers in Asia and elsewhere. But many countries in Asia have still been in the throes of lockdowns and other coronavirus-related restrictions, constricting their ability to meet demand.

Meanwhile, global labor shortages, often the result of people leaving the workforce during the pandemic, have thrown further obstacles in the way of producers. The bottlenecks will constrain manufacturing output well into next year, hurting a sector that had until recently powered the global recovery.

Supply-chain disruptions have helped push inflation to multidecade highs in the U.S. and parts of Europe, weighing on consumer spending. Supply constraints for manufacturers are squeezing margins and pushing up consumer prices. Elevated inflation rates have already put pressure on central banks, including the Federal Reserve, to start scaling back their aggressive pandemic stimulus policies, a further headwind to global growth.

Global: The global economy has continued to face a flurry of issues. COVID-related growth disruptions have been persistent, while regulatory changes and property sector challenges have weighed on China's economy. Europe has handled the wave of the highly infectious Delta-variant well, outperforming expectations in the first half of the year. In contrast, emerging markets (EM) with insufficient vaccine access and healthcare infrastructures have been devastated by its effects. The COVID threat to the EM economies will persist in the near term. Against this backdrop, the outlook for the global economy has softened, and risks around the global growth forecast have remained tilted to the downside. Global growth is expected to be around 5.8% in 2021.

China: China's economy has slowed in recent months, as COVID-related restrictions have weighed on services and retail activity in particular while regulatory changes and real estate disruptions have more recently held back activity.

China's economy has experienced an increase in leverage over the past decade including, importantly, an increase in corporate leverage. While a corporate debt crisis in China has not materialized to date, recent developments related to Evergrande, one of China's largest property developers, suggested the likelihood has risen. At the same time, regulatory changes have escalated Evergrande's default risk. A default or disorderly collapse of Evergrande would have negative implications for China's real estate industry and for the broader Chinese economy. Furthermore, it is possible that Evergrande's financial problems may not be isolated, as China's system-wide leverage—including its non-financial corporate debt levels—have been quite elevated.

That said, Chinese elevated corporate debt has been a vulnerability to China's economy and a moderate risk to the global economy, but not likely a problem that will cause the next Global Financial Crisis a-la 2008. A collapse in China's real estate market, were it to occur, is not expected to prompt another Lehman Brothers moment. This has been, in part, because China's foreign debt exposure is currently much lower than what the U.S. foreign debt exposures were before the 2008 Global Financial Crisis.

Outlook: The downward adjustment to the U.S. outlook does not negate a solid rebound of 5.5% for 2021. Looking ahead to 2022, growth is expected to follow through at a solid 4.0% rate as more activities normalize while the pandemic recedes. Continued above-trend growth in 2023 is expected to drive the unemployment rate slightly below its pre-pandemic low to 3.4% enabling rate hikes by the Federal Reserve.

Downside risks stem from the ongoing uncertainty of the virus and variants, along with the possibility that supply-side constraints could weigh more heavily on production and consumption. On the upside, Americans have built up a substantial cash cushion, which could drive spending higher than we assume. Fiscal policy presents both upside and downside risks. It is assumed that Congress passes the Infrastructure Investment and Jobs Act. Any misstep here would therefore present a modest disappointment. On the other hand, Democrats have even larger plans for social spending, funded by tax increases. This could present a boost to growth next year depending on the final details. The Federal Reserve will likely maintain the current low-rate environment until the final quarter of 2022. At that point, it is expected to initiate rate hiking cycles, with the federal funds rate reaching 2.0% by 2024.

Over the coming quarters, government yields are likely to continue to rise. This rise will be driven by three factors: first, markets will continue to solidify a higher policy path for the federal funds rate; second, the Federal Reserve will end net-new bond purchases over the coming quarters; and third, lingering inflation will cause investors to demand higher compensation for inflation risk.

This Newsletter was produced for Atlantic Union Bank Wealth Management by Capital Market Consultants, Inc.

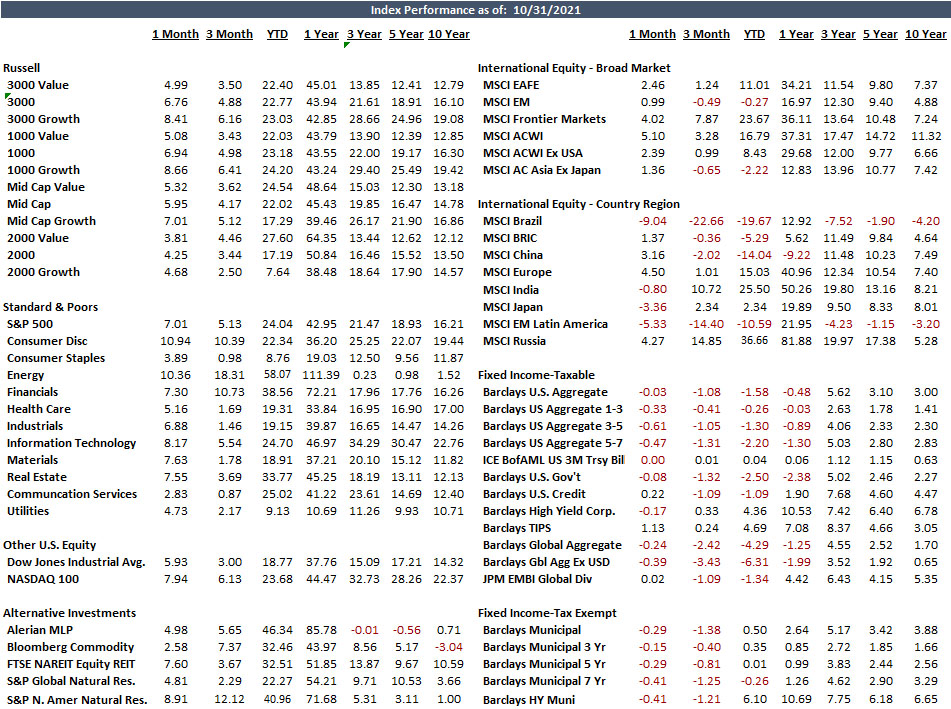

Sources: Department of Commerce, Department of Labor, Morningstar, Bloomberg, Federal Reserve, John’s Hopkins University, National Bureau of Statistics China

Disclosures:

Past performance quoted is past performance and is not a guarantee of future results. Portfolio diversification does not guarantee investment returns and does not eliminate the risk of loss. The opinions and estimates put forth constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Securities are not insured by FDIC or any other government agency, are not bank guaranteed, are not deposits or a condition to any banking service or activity, are subject to risk and may lose value, including the possible loss of principal.

Atlantic Union Bank Wealth Management is a division of Atlantic Union Bank that offers asset management, private banking, and trust and estate services. Securities are not insured by the FDIC or any other government agency, are not deposits or obligations of Atlantic Union Bank, are not guaranteed by Atlantic Union Bank or any of its affiliates, and are subject to risks, including the possible loss of principal. Deposit products are provided by Atlantic Union Bank, Member FDIC.